“Economics is really about two stories. One is the story of the old economist and younger economist walking down the street, and the younger economist says, ‘Look, there’s a hundred-dollar bill,’ and the older one says, ‘Nonsense, if it was there somebody would have picked it up already.’ So sometimes you do find hundred-dollar bills lying on the street, but not often—generally people respond to opportunities. The other is the Yogi Berra line ‘Nobody goes to Coney Island anymore; it’s too crowded.’ That’s the idea that things tend to settle into some kind of equilibrium where what people expect is in line with what they actually encounter.”

― Paul Krugman

I love this quote. These two jokes do sort of describe economics, at least what you might call “pure” or celestial economics, where there are no real world frictions to worry about. If we add frictions to the mix we get terrestrial economics, the economics of the real world.

Krugman’s first joke gets at the way economists think about information. It’s essentially epistemology, about whether to believe something is true. The second joke is about behavior, about how we model the response of people to changes in their environment. At the end I’ll add frictions, and try to give you a sense of how economists like me think about the world. So here’s my 4-minute course on economics.

1. Information: Imagine a giant encyclopedia, written in Japanese. It contains a vast amount of information about the world. But to read it one must first learn Japanese. By learning economics we are able to read an enormous amount of information from prices, if we assume that people are rational utility maximizers. Thus if conventional Treasury bonds yield 7% and indexed bonds yield 3%, we can infer that optimal forecast of inflation is 4%. If that were not true, there would be $100 bills lying on the sidewalk for investors to pick up.

Here’s another example. Suppose there’s a neighborhood of cookie-cutter homes on the Irvine/Lake Forest boundary, here in Orange County, CA. If we compare two similar houses on each side the border, we can infer the difference in value that people see in living in each city, capitalized into the home value (actually land value.) Most likely, this reflects differences in the perceived value of the two school systems, with Irvine viewed as superior. If the price gap didn’t reflect perceived amenity differences then homebuyers would take advantage of any mis-pricing.

Here’s another example. Assume that Mexican farm workers in California earn $11/hour on average while Central American farm workers in California earn $10/hour on average. We can infer that the Mexican farm workers are probably about 10% more productive, on average, otherwise California farmers would choose to hire Central Americans, not Mexicans. Again, no $100 bills on the sidewalk.

The economy contains billions of such pieces of information, all embedded in prices, for those who know how to “read economics”. It’s like a giant encyclopedia.

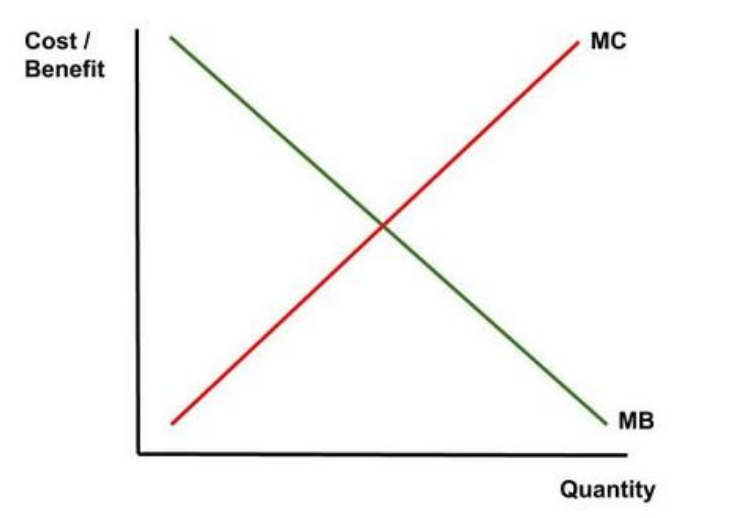

2. Behavior: Economists assume that rational people will keep doing X up until the point where the benefit of one more (marginal) unit of X no longer exceeds the marginal cost of X. This is the “equilibrium”. X could be any activity: units consumed, hours worked, dollars invested, etc.:

Urban planners often suggest that expanding highways does not reduce traffic congestion. That’s wrong. If you widen a highway, more people will travel on the highway. That part is true. But traffic congestion will be reduced; indeed it must be in order to induce more people to travel on the highway. Why do urban planners get this wrong? Because they noticed that traffic did not seem to improve when places like Orange County built more highways. But that’s because both lines were shifting at the same time, as Orange County’s population was growing rapidly when it was building new roads. It is still true that, other things equal, building more highways reduces traffic congestion. Recently, Orange County’s population stopped growing. Now if they were to build more highways in OC, it really would reduce traffic congestion.

Or consider how firms respond to a change in the cost of inputs. Most students understand that firms will respond to cost increases by raising prices, but often fail to see that firms will respond to price decreases by cutting prices. But the model is symmetrical; a shift up in the MC curve has the opposite effect of a shift downward, even for a 100% monopoly. In both cases, cost curve shifts move the optimal output point, which requires a price change. And we know that firms don’t want to leave $100 bills on the sidewalk.

So that’s celestial economics in a nutshell. It describes a world where inefficiencies should be quickly eliminated, as utility maximizers do deals to improve efficiency and share the gains. No $100 bills left on the sidewalk.

3. Frictions: Here in the real world, things don’t work so smoothly. One friction is transactions costs. In principle, inefficiencies related to externalities (pollution, etc.) and monopoly could be eliminated through negotiations. Pollution victims could bribe factories not to pollute. Monopolies could negotiate perfect price discrimination with consumers. But such negotiations are often costly and hard to do, for all sorts of reasons. Another friction is sticky wages and prices, which result in nominal shocks having real effects. Bad real effects, such as high unemployment. Another friction is illiquidity, which explains why the TIPS spread may not perfectly measure the public’s inflation expectations. TIPS are less liquid, and hence less desirable. Furthermore, information is costly. So there may be a few $100 bills on the sidewalk because no one spent the resources to look for those $100 bills. And there’ll be lots of coins on the sidewalk.

Left leaning economists focus more on frictions. Right leaning economists focus more on celestial economics. I’m somewhere in the middle, but definitely leaning to the right.

READER COMMENTS

Lance

Mar 5 2021 at 3:29pm

The problem with a lot of the left-leaning economists is that they seem to go, “Well if there are these frictions already, so let’s add more!” Leftists of course typically want to burn markets down (ignoring that market dynamics pop up just about everywhere as an emergent property regardless of your belief in them).

Just because Newtonian physics was far from complete didn’t mean it wasn’t extraordinarily useful (and mostly accurate at human levels).

robc

Mar 5 2021 at 3:42pm

You missed one part of the road situation in #2. Even with static population, adding more lanes will lead to more people driving vs other options (bus, train, private helicopter). I dont think that is enough to entirely fill the new lane, but it is a part of it. Growing population is the bigger factor, of course.

Plus, even within a static population, it will shift the location of the population, as people can live further from destinations.

Scott Sumner

Mar 5 2021 at 6:54pm

You said:

“Even with static population, adding more lanes will lead to more people driving vs other options (bus, train, private helicopter).”

I said:

“If you widen a highway, more people will travel on the highway. That part is true.”

So no, I did not miss that part.

Jon Murphy

Mar 5 2021 at 3:50pm

What I like about the UCLA-style of economics (Alchian, Demsetz, Hirshleifer, Walter Williams, David Henderson) is that the frictions themselves are important, too. Simply because frictions exist does not imply that the market has failed in any sense. For example, if there is some externality where the net benefit of reducing it is, say, $4 (so, there is a Pareto-improving outcome that does not come about), but the transaction costs needed to overcome are $10, then even if some agent can overcome transaction costs, the transaction would not take place. The cost of transacting is simply too high.

I think left-leaning economists are right to focus on transaction costs. But, like most people, they misunderstand the lessons from Coase. Frictions do not in and of themselves justify intervention in the economic process.

Thomas Hutcheson

Mar 7 2021 at 7:24am

So why don’t you set them right on what intervention are recommendable once at proper estimates of transaction costs of the intervention properly taken into account and how to design them?

Perhaps I misunderstand you, but you seem to be saying that no policy intervention in the case of an externality can possibly have lower transactions costs (given among other reasons public choice problems that prevent designing the lowest cost intervention) than the externality it weeks to overcome.

Jon Murphy

Mar 7 2021 at 12:39pm

I do. Frequently. For example, here.

Thomas Hutcheson

Mar 10 2021 at 6:28am

No, this looks like an extended diagnosis of why proposed interventions may not be optimal.

I was looking for a worked out (sketched out) example applying your theoretical objections to a specific proposal to show that it is in fact not optimal and then showing how to make it less bad.

Frank

Mar 5 2021 at 6:29pm

… if we assume that people are rational utility maximizers.

Nah, we observe their behavior and infer that they are [or are not] maximizers of a nice function. Apparently they are.

Scott Sumner

Mar 5 2021 at 6:55pm

It’s quicker to just assume. 🙂

HH

Mar 6 2021 at 12:07pm

“Now if they were to build more highways in OC, it really would reduce traffic congestion.”

Briefly. Then behavior adjusts and travel times go back to where they’ve always been, or get worse. You may get a different answer if you define congestion differently than the average person, but evidence against the above statement is near-universal.

HH

Mar 6 2021 at 12:13pm

Empirical evidence:

https://www.strongtowns.org/journal/2021/3/3/the-fundamental-global-law-of-road-congestion

Scott Sumner

Mar 6 2021 at 5:46pm

Citing the Katy freeway is not very persuasive, as that area is booming. Try reading my post again; I think you missed the point.

HH

Mar 7 2021 at 7:31am

There’s a lot more than Katy in that piece, and you know that. I’m not sure why you’re insisting that behavior wouldn’t change in response to a lower price of commuting until the price rises again.

HH

Mar 7 2021 at 7:52am

It works in both directions. Take a look at the travel time stats in Detroit and Buffalo. They dropped with the population drop … and then rebounded to where they’ve always been. Any change is temporary, and behavior then adjusts.

Scott Sumner

Mar 7 2021 at 12:19pm

You said:

“I’m not sure why you’re insisting that behavior wouldn’t change in response to a lower price of commuting until the price rises again.”

I said behavior would change. I said it would induce more people to drive. I really don’t think you understood the post.

You need to use marginal analysis. Draw it out as a graph, and shift one line.

MarkW

Mar 6 2021 at 1:36pm

And yet there are places that have enough road capacity so that traffic is much less congested than it is in southern California. If you think it’s a law that traffic automatically expands to fill capacity, how do you explain the fact that these other less congested places continue to exist?

HH

Mar 6 2021 at 4:58pm

They are populated by people willing to pay a lower price, in terms of time and congestion.

KevinDC

Mar 6 2021 at 3:31pm

I very much like the metaphor of an encyclopedia written in a new language you need to learn – in this case, the language is economics.

Understanding the language really is necessary for understanding the ideas too. It makes me think of times when someone talks about a change in supply, and I (or others) point out that what they’re actually talking about is a change in quantity supplied, not a change in supply. (Or change in demand vs change in quantity demanded.) To someone who doesn’t understand economics, this probably sounds like some sort of nitpick akin to “you shouldn’t end a sentence in a preposition.” But the difference between moving along a curve and shifting a curve is really big and they have very different implications. Statements about one situation don’t translate to the other.

That in turn reminds me of when someone was trying to argue that restricting the housing supply doesn’t increase housing prices. He tried to support his case by pointing to places where new construction was occurring rapidly, and prices were still rising. Of course, anyone who tried to use that reasoning would flunk Econ 101, and it was embarrassing to read. But it was just him making the same elementary mistake you point out by not realizing “both lines were shifting at the same time.” To continue the metaphor, it would be like someone who thinks they’ve learned to speak a language after memorizing a few phrases phonetically. It’s just not a substitute.

Scott Sumner

Mar 6 2021 at 5:47pm

Good points.

David Seltzer

Mar 8 2021 at 3:50pm

Scott, Clearly explained. Thinking about congestion. Congestion has a time component and how time is allocated is important. If there are more cars per mile on the Interstate 405, and the average time from point A to Point B is reduced, marginal benefit is increased. If time from to A to B increases, doesn’t the MC curve shift up and to the left? Reducing the benefit of increased traffic lanes?

Comments are closed.