On February 5th I wrote:

I suspect that the stock market disagrees with experts who predict a global pandemic:

The Wuhan coronavirus spreading from China is now likely to become a pandemic that circles the globe, according to many of the world’s leading infectious disease experts.

It will be interesting to see who turns out to be right. I don’t have a strong opinion either way.

The fact that I didn’t sell my stocks, however, suggests that I leaned toward the “market” view. I was wrong.

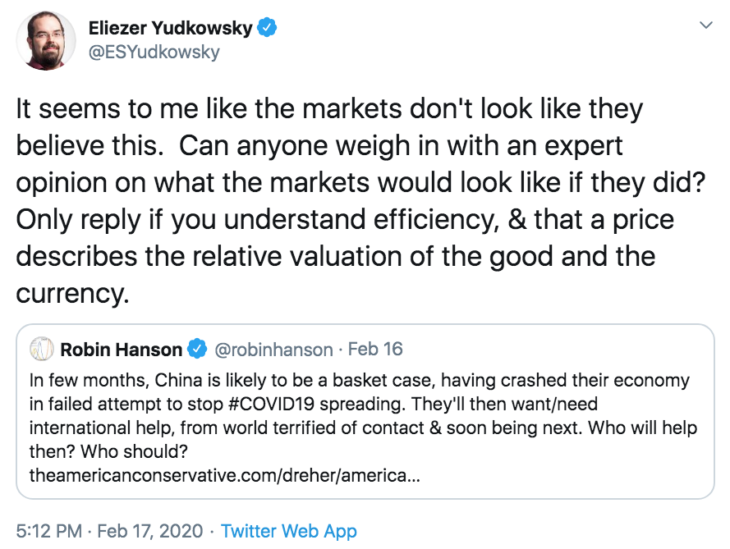

Craig Fratrik directed me to a discussion in the “rationalist” community, where a number of individuals did believe the coronavirus would become a big problem in the West. This February 17 Eliezer Yudkowsky tweet is interesting:

And here’s the S&P500 after his tweet:

Eliezer Yudkowsky has been a longstanding believer in the Efficient Markets Hypothesis, and by mid-March he had begun to wonder whether there were certain types of unusual events where markets would not respond in an efficient manner. (Rationalists like Yudkowsky update their beliefs about the world as new information comes in, whereas many non-rationalists try to make new information fit their preconceived ideas.) Indeed Yudkowsky even made some money by investing at the very low point of the stock market, on March 23.

Yudkowsky also pointed out that (rationalist?) Wei Dai made a lot of money shorting the market, in anticipation of the coronavirus crash.

Craig Fratrik also directed me to a post in another rationalist blog, which described selling stocks in the belief that the markets were wrong about coronavirus. It seems like the rationalist community was ahead of most of the rest of us.

[I don’t follow this group closely, so someone let me know if I’ve misrepresented the rationalist community in any way.]

Should all of this make us less likely to believe in the EMH? I’d say yes, but only a little bit.

This is not the first time something has happened that seemed inconsistent with the EMH. Consider the October 19, 1987 stock market crash, where the Dow fell 22% on a light news day. Nonetheless, I’ll argue that the EMH remains more useful than it appears, despite the poor performance of the markets in this case, or in October 1987.

Let’s start with the tweet at the top, where Yudkowsky retweets a Robin Hanson tweet, which summarizes a Rod Dreher article from February 15th. A very pessimistic article.

Most of the Dreher article consists of quotes from an anonymous American living in China. [Yes, we are now 4 layers deep in this process.] This American gets the big picture right (a global pandemic on the way) but gets wrong some of the details. For instance:

With respect to the disease itself, I don’t think this disease can be stopped anything short of supernatural means. Infections continue to soar, even under military-enforced quarantines that have been in place for almost a month. You have to see the Army response here to believe it, and yet nothing has worked. You mercifully haven’t had many cases there, yet, but I fear that you’re just six or seven weeks behind where we are in China, and four to five weeks behind Japan. Only a miracle can stop it, and that’s what we need to be praying for. If you’re a man or woman of faith, get some more. If at some point you left it or lost it, go back to where you saw it last, and pick it up again.

In fact, the epidemic in China was halted very quickly after that tweet, without “supernatural means”. I don’t want to sound like I’m nitpicking, as this anonymous American was right on the big issue–Americans weren’t taking this anywhere near as seriously as they should. But being right about the public policy implications is not the same as being right about the implications for the EMH.

I recall thinking in late February that since China had quickly gotten this under control, then more developed countries that had all the advantages of being able to watch what the Chinese had done would be able do the same. That was clearly wrong, but it’s still not obvious to me that it was an irrational belief, given what we knew at the time. After all, previous diseases such as SARS didn’t have a dramatic impact after they left China. Yes, the coronavirus had a much higher “R0” (reproduction rate) than SARS, but again, China was quickly controlling the coronavirus epidemic, even after it had already infected tens of thousands in Wuhan and elsewhere. The US had only 15 known cases on February 20.

In a sense, this is similar to the US housing bubble and crash. In retrospect, it looks obvious that the housing market was unsustainable in 2005-06. But recall that other countries with similar “bubbles”, such as Australia, New Zealand, Canada and the UK, never had the sort of crash that the US experienced. It’s only in retrospect that the US housing crash seems obvious.

I predict that community transmission of coronavirus in Australia and New Zealand will be down close to or at zero by mid-May. (Someone remind me of this prediction in mid-May.) Unfortunately for those two countries, the world as a whole will still have a big problem in May, and thus the economies in those two lucky countries are still likely to be severely depressed. But as of mid-February, it was not obvious (to me or the markets) that a virus the US and Europe would be unable to control would be relatively quickly controlled in Australia.

For me, the claim that the EMH is “wrong” is equivalent to the claim that it is no longer useful. But is that true? I very much doubt that markets will under-react the next time the world is faced with a coronavirus-type threat. Indeed I suspect if there is irrationality, it’s equally likely to be in the direction of overreaction. So I don’t see how this particular market error will help me going forward. How do I trade in the future on the knowledge that the market blew it in the case of the coronavirus?

Undoubtedly, there will be future events where a select few well-informed people will see the truth more clearly than the market consensus. But how will I know when that situation is occurring, as compared to a situation where well-informed people wrongly believe they are smarter than the market? Does this example tell us how to know when to trust the experts over the markets? I don’t see how.

READER COMMENTS

blink

Apr 13 2020 at 2:19pm

Yes, this is a data point that vies against EMH. Still, it is hardly fair to judge ex post. Based on what we knew at the time, the market may have been priced according to an appropriate measure of risk, say 50/50 on serious vs. mild. Later weeks just revealing the coin flip to be tails (serious) and the market fell. But had the coin flip come up heads (mild), the market would have risen. In *both* cases, there is a large ex post adjustment that makes the ex ante assessment and EMH look “wrong” but this is misleading. All we can say for sure is that the market *quickly* responded to new information as it developed.

bill

Apr 13 2020 at 3:15pm

I totally agree with your conclusion. Any time the market it gets it wrong, the market learns. This can be a lonely position to defend at cocktail parties. Lol.

Anon.

Apr 13 2020 at 3:19pm

I move in “rationalist” circles and based on the talk around that time I shorted before the crash…but I only took a very small position. My belief in the market’s efficiency was too strong (at the time) to make a brave move.

Philo

Apr 13 2020 at 3:45pm

The failure of the market perfectly to predict the future does not refute the EMH.

Scott Sumner

Apr 13 2020 at 5:45pm

I agree.

Matthias Görgens

Apr 14 2020 at 9:05pm

Yes. The bigger challenge to the EMH here is not the failure to predict, but the community of people who predicted better based on publicly available information.

It’s not the death of the EMH. But it is a challenge.

Thomas Sewell

Apr 18 2020 at 9:41pm

In order for that to have anything to say in relation to the EMH, wouldn’t that group of people need to predict multiple (i.e. more than one) similar effects on the markets in advance?

Consider that at least one person I’ve seen mentioned in the rationalist community who “called” this pandemic right also “called” the last three the same way in advance…. but incorrectly because they never exploded like this.

Sometimes people are just getting lucky that reality lined up with their prediction, rather than being consistently more correct than the masses reflected in the markets.

nobody.really

Apr 13 2020 at 3:53pm

Not following this. What is the hypothesis? What was the test? Was there a control group?

As far as I can tell, Sumner observed that some people predicted that the stock market would move in a certain direction–and it subsequently did. Yet on any given day, I expect we could find SOME people predicting the market will rise or fall, and roughly have of them will be right. What conclusions should we draw from that?

To defeat the EFT, we’d need evidence that certain people REGULARLY out-guess the market (perhaps as evidenced by their vast wealth from trading) without the benefit of insider information. So–do we have such evidence? Or are we just cherry-picking data?

Scott Sumner

Apr 13 2020 at 5:42pm

I agree.

foosion

Apr 13 2020 at 9:37pm

Of course there are some who have vast wealth from trading. The harder question is whether this is due to skill or luck and the answer appears to be that we don’t have enough data to tell.

For an individual investor, EMH is essentially irrelevant – just buy broad low cost index funds.

Using the market to determine whether there’s a real threat of a pandemic and whether we should prepare does not sound like an optimal strategy.

Matthias Görgens

Apr 14 2020 at 9:07pm

The EMH is a big part of the reason why just buying the index and not even worrying about checking the news the morning before you buy works so well.

AMT

Apr 13 2020 at 4:43pm

I don’t think you can really knock the EMH too much here. By definition, stock prices incorporate all public information about future expected profits. The fact that many people didn’t expect the virus to cause as big of an impact as it did is perfectly consistent with that. Others in the minority who disagreed were just that, a small minority. Anytime you have superior information to most other investors, you can profit. That’s exactly what EMH says.

If anything, I think the most important missed prediction was not the spread of the virus, but the economic shutdowns that have spread across the world. If you think about it, just how much would you expect a virus that kills a small percentage (maybe 3-5%?) of the people that are infected, affect the global economy, especially when you consider that the vast majority of those deaths are among the already retired? You’d think that GDP wouldn’t decrease much at all, and GDP per capita could actually increase. I was not surprised to see the virus spread quickly, but didn’t expect the a massive (over?)reaction to the virus. That is the zeitgeist we live in.

I wouldn’t have been surprised at all to see Trump shut down international trade, but didn’t expect to see such a massive domestic shut down as well, for a disease that kills such a small number (0.1%? citation needed) of people under 50 that get infected. This virus is nowhere near ebola, but it feels like the response is getting close to what would be justified for that kind of disease.

So, what I actually find much more surprising is how the dow went back up to 23k so quickly, in the midst of massive unemployment numbers and with a whole lot of uncertainty about just how long these shut downs will continue to affect the economy. There hasn’t seemed to be much good news that would change that outlook since then, but apparently investors are for some reason very optimistic the shutdowns will be quite brief! And not recur! So, I think if the dow drops back under 20k in the next few months, that’s a much better reason to discount EMH, because the significant risk of a massive hit to the economy is so much more obvious now.

Scott Sumner

Apr 13 2020 at 5:42pm

If in February the market had known that by early April you’d have 2000 deaths a day in the US, I assure you that it would have been much lower.

AMT

Apr 14 2020 at 10:06am

Then explain why the death rate and stock market index trends are exactly the opposite from March 23 to now. Are you saying people expected far, far more deaths than we have actually had? So every day since then, as deaths have increased up to 2k per day, has been a surprising relief? That is literally how you must be interpreting the stock market data…

https://www.nbcnews.com/health/health-news/coronavirus-deaths-united-states-each-day-2020-n1177936

So compare that with the dow jones.

Again, my point was that even 2k deaths per day is not that many in the grand scheme of things.

https://www.cdc.gov/nchs/fastats/deaths.htm

Scott Sumner

Apr 14 2020 at 2:09pm

It’s not the deaths themselves, it’s what they imply about a shutdown of the economy.

AMT

Apr 15 2020 at 9:53pm

That’s what I first said…then your first comment was about deaths…

Matthias Görgens

Apr 14 2020 at 9:12pm

The Rationalist community used publicly available information to make their predictions. By and large they didn’t have better information.

That’s the challenge to the EMH.

We have to acknowledge challenges, even if we don’t believe they invalidate our ideas, yet. An idea that’s can not be challenged by anything happening in the world doesn’t say anything useful either.

Luckily, some of them traded. And if they notice that they can predict things better than the market time after time, they’ll trade even more, helping the markets incorporate that new way of digesting information.

danny

Apr 13 2020 at 4:56pm

But for the EMH to be truly wrong wouldn’t a person or group of people have to consistently beat the market? Maybe Eliezer just got lucky this time. The market will always be “wrong” to some degree and there will always be individuals that did a better job at various points in time. As I think you would normally say, “This is a prediction of the EMH”. Only if the same individuals outpredict the market repeatedly would the EMH be called into question.

Aleksander

Apr 13 2020 at 4:57pm

Many people who are now rationalists, also made some money on Bitcoin back in the day. Those who were able to benefit both from that opportunity and this one, clearly beat the market in a real sense (as in, it wasn’t just luck).

Scott Sumner

Apr 13 2020 at 5:44pm

It’s hard to be certain that luck was not involved. Bitcoin became a successful investment, but not a successful “money”. So what exactly did they predict?

robc

Apr 14 2020 at 2:00am

Bitcoin has failed as money because it is too good at being money.

Gresham’s Law.

Matthias Görgens

Apr 14 2020 at 9:23pm

Gresham’s law doesn’t work like that.

Gresham’s law says that if the king compels people to accept various kinds of money at the same face value, the bad money will ‘win’.

In the absence of such force, people will accept the bad money only with a discount. And the good money usually wins.

You can see lots of historical examples. For example when people use USD when their local currency is bad.

Or in previous centuries, you can see that even from the same mint run by the same ruler, you got coins of different quality: the smaller denominations for local circulations were much more debased than the bigger ones meant for international trade. That’s because there was more coercion in the former and more competition in the latter.

robc

Apr 15 2020 at 10:31am

The logic follows the same though.

If I have both btc and usd and someone accepts both, I would prefer to spend the declining asset (dollars) instead of the increasing asset (btc, maybe). So the dollars will be used and the btc would be held as an investment instead of spent as currency.

Its the same reason we don’t make purchases with stock certificates.

The good currencies (btc and stocks) get driven out of commerce and are held as investments, while the bad currencies (dollars) get spent as fast as possible before they can decline in value.

Aleksander

Apr 14 2020 at 12:37pm

They predicted that they would earn money by investing in Bitcoin, rather than other investments. Honestly, the returns on that investment are so incredible (100x-1000x) that it’s unlikely to be luck, even if that’s your only datapoint. Or are there 1000 parallell universes where they invested in other risky commodities whose price went to zero?

If they in addition to that also managed to earn money on coronavirus, I think it’s hard to argue that it’s pure luck (in the “Every year half of all investors end up with a profit, and Warren Buffet is just the lucky one who has done so x years in a row” sense).

Scott Sumner

Apr 14 2020 at 2:10pm

That’s like saying the returns on a winning lottery number are so high that it can’t be luck.

James

Apr 13 2020 at 5:06pm

The EMH answer to your question in the title is that the covid 19 scenario we actually observe is a single draw from a distribution, but the market price on any day is a probability weighted average over the entirety of that distribution.

One non-EMH view is that market mispricings get corrected very quickly when the important variables are the ones finance people pay attention to: earnings, growth prospects, etc. When other variables such as disease become the most important, markets become mispriced because finance people are not paying as much attention.

Can you clarify what you mean by efficiency?

Here is the argument I so often see:

If markets are efficient, asset prices will be unpredictable.

Asset prices are unpredictable.

Therefore markets are efficient.

As popular as this argument may be, it is the fallacy of affirming the consequent. There are other conditions besides efficiency that would lead to unpredictable prices and it is a leap of logic to infer market efficiency from unpredictability alone. If market prices were determined by a committee that secretly spun a big wheel in a back room, they would be random and inefficient and EMH people would probably still point to the unpredictability as evidence of efficiency.

As to the usefulness of efficient markets theory: If markets are efficient, then markets are unpredictable and so also is the return (before costs) to any sort of market timing strategy. If EMH is true, then there is no reason not to try to time the market. Specifically, the EMH cannot even distinguish between a regularly rebalanced 60/40 allocation to stocks/bonds, buying at 60/40 and holding without rebalances, and a strategy which leads an investor to hold only stocks 60% of the time and bonds 40% of the time. And yet among EMH believers it is common to see recommendations similar to regularly rebalanced 60/40 and exceedingly rare to see recommendations of dynamic strategies or buy and hold without rebalancing.

Matthias Görgens

Apr 14 2020 at 9:32pm

The EMH has some other neat consequences.

For example, if you discover a new piece of information about Amazon that no one else knows, you can immediately go and trade on it. You don’t have to comb through all the other public information to decide, because the market price already incorporates them.

That being said there’s no single EMH. It’s a family of hypothesis that’s commonly grouped by their strength.

My favourite formulation goes like: by the time you as a retail investor read about something in the news, the people at the hedge funds and Goldman Sachs who obsess about finance full time will have already traded on it.

(Note that the good trades by the rationalists challenge even this relatively weak version!)

Chris

Apr 13 2020 at 6:02pm

I’m going to over-reach a bit, but this post reminds me of one Scott made just over 2 years ago, also about China: https://stageeconlib.wpengine.com/archives/2018/03/the_west_was_ri.html

In each, Scott basically makes an argument in the form of “others (pundits/experts) are now claiming that present events disprove, or at least ought to encourage a reconsideration of, a general principle that I have held for quite a while.” In each case Scott suggests that he’s likely to be proven (more) right in the long run. In each case, this seems to require lengthening the time horizon and working around potentially disconfirming evidence.

I think Scott was wrong in 2018, and his reply that we needed 20-30 more years was a tacit admission that they only way he could be right was to re-configure the time horizon. However, in both that case and this case, I credit his good faith and willingness to directly present evidence cutting against his view. In fact, I great admire his intellectual honesty.

I am not an EMH advocate but I will grant that it is going to come in for unduly harsh criticism from some who just happened to be right. EMH isn’t gospel, but it’s not totally bunk, either. Long run, and all that.

That said, the current pandemic isn’t a black swan. Or, at least, is was entirely predictable that states would seek to avoid looking like Chicken Little given that past possible pandemics didn’t hit in the U.S., and that markets are generally averse to looking like Chicken Little at all. There are multiple optimism biases at work.

There is a reluctance in some quarters to acknowledge that the states that are handling this best not only have past experience (with SARS, etc.) to fall back on, but also have prioritized state capacity (I don’t mean it exactly that way) in a manner that doesn’t mesh with what would be advocated by an economic, “let’s remove redundancies and maximize efficiencies by outsourcing supply” approach.

MJ

Apr 13 2020 at 6:50pm

Most of the stock market’s value is traded by a relatively small group of people. I’m sure there were lots of traders that identified the gap by mid Feb or earlier and they didn’t move prices at all.

Phil H

Apr 14 2020 at 2:45am

As others above – this post seems to be using “EMH” to mean “wisdom of crowds (as reflected through a market),” but I don’t think that really captures it…

Also, I think this casual wording is a bit off-base: “…the big issue–Americans weren’t taking this anywhere near as seriously as they should…”

America isn’t necessarily “the big issue” any more. And in this debacle, America’s failure to handle it well makes the country significantly less important. The big issue now is whether the rest of the world starts to look to China or to Taiwan for pointers on how to get it right.

Scott Sumner

Apr 14 2020 at 2:11pm

I sure hope it’s Taiwan.

Mark Z

Apr 14 2020 at 8:05am

I’m not sure it was rational, with available information, to predict disaster of the scale as it has happened much earlier than mid-February. Testimonies of foreigners living in China may have turned out to be prescient this time, but in general, that doesn’t seem like very solid data to make decisions off of. That some people, even rational people, were predicting catastrophe that early doesn’t necessarily prove it was the most likely scenario given what was known at the time.

Alternatively, if markets mostly ‘reason’ heuristically, then the likelihood of extremely rare, complicated events with which we have little experience may be very difficult for markets (or people) to assess. Maybe extremely rare events are a sort of boundary condition for EMH? The complexity of the relevant information also seems like something that would affect the alacrity of the market’s response. For example, imagine some mathematician proves an extremely difficult theorem that will, in the long run, lead to enormous technological improvements. Will markets react instantaneously like they would to an announcement by the Fed whose implications are well known? Maybe not: they have to wait for the hundred or so people in the world who could understand the proof to thoroughly dissect it and debate it among themselves before ultimately affirming the proof. Even though the relevant information – the proof itself – is right there, its inaccessibility means it could take years before it really becomes ‘generally available information’ that the proof is correct. And if many people have falsely claimed to have solved the proof in the past, the market’s prior may be to assume the latest proof is probably incorrect. The relevance of this analogy to covid19 of course depends on the idea that the hypothetical epidemiological debate over how bad it would get as of 2-3 months ago was sufficiently complex that it would require a few weeks ‘processing time’ (certainly not as long as the couple years it took for the mathematical community to confirm the proof of the Poincare conjecture). If of course it was just basic epidemiology that the outbreak would get really bad globally then complexity doesn’t help explain things.

Michael Rulle

Apr 14 2020 at 10:18am

Professor Sumner picks a good time to reflect on the EMH, for reasons he has outlined. It is always a smart thing to do about any accepted belief about the world.

My thoughts on the matter. It is called the Efficient Market Hypothesis. For all practical purposes its major prediction is it is not possible to outperform markets on average and over time, except by luck. I don’t believe it ever has implied that “after the fact” all past prices were correct——which all critics of the theory seem to focus on. The EMH is not a fortune teller.

It has been critiqued as bad on scientific method (not the same thing as being untrue) and that critique is valid. When Fama and French “discovered” factors (value, quality, growth and others) they did so after it was shown that certain strategies outperformed the market as a whole. So they needed to update EMH after the fact (a kind of a no-no-in science) in order for the evidence to fit the EMH theory. However, “out of sample” we have discovered these factor based indices are also hard to beat as EMH would predict.

This raises other complexities however. Have there been timers who have known when to weight various factors over others? I don’t know, but I am guessing there are far less studies on this.

Another interesting question—-just what exactly is the market? The EMH was originally designed for equity markets—-at least all studies were about equity markets. But approximately (and believe me, depending what one counts this number can be vastly different) 60-65% of publicly trade securities globally are fixed income and 35-40% equities. Shouldn’t this be the “market” against which one should be measured——it is, after all, the cap weighted market which the EMH predicts cannot be outperformed on average and over time.

Finally, what does out perform mean? Absolute returns or risk adjusted returns? Many more issues can be raised. But it is clear the EMH is not a fully flushed out theory like, for example, General Relativity.

So for simplicity’s sake, let’s just look at a subset of the Capital Market that most people imply when discussing EMH——the most liquid equity market in the world —the S&P 500. Or maybe the Russell 2000—which as a whole is less liquid.

Is there incremental evidence that the S&P 500 has in some way put a dent in EMH as a function of its reaction to the coronavirus? I really don’t think so. I do believe other times are better candidates —but will ignore for now.

Again, the EMH says it is hard to outperform it without luck. It says nothing about the nature of the information which drives the price. Information has been wildly uncertain and volatile. Also, dispersion and correlation has been high as they always are in times of crisis. Plenty of opportunity to outperform and underperform in the short run. We should expect to see a higher percentage of active funds to both outperform and underperform by more than usual. And we will see if better results than we expect from randomness will occur. My guess is no.

I

Pierre Lemieux

Apr 14 2020 at 11:19am

Two comments on this interesting post, Scott.

First, I share your general view on EMH. I like to think that all available information is incorporated in financial asset prices, but that there may be some unavailable information or that the available information may not be interpreted correctly (because of a false information cascade, for example). But I suspect (and it bugs me) that this little theory is not very solid.

Second, you write:

Here, I would suggest that there may not have been enough public-choice analysis in your thinking! (With hindsight, who could have thought that bureaucrats like the Surgeon General, who was fighting tobacco, or the FDA, who was fighting vaping, would be able to fight a real epidemic?)

Scott Sumner

Apr 14 2020 at 2:14pm

Yes, in hindsight that’s pretty obvious. I did not know how inept we were at testing for the disease or buying surgical masks on the global market.

Ash

Apr 14 2020 at 2:46pm

Scott Sumner are you familiar with the famous P vs NP problem within mathematics and computer science? Since the EMH states that all prices are a reflection of all present information this supposes that every computational problem in the price can be solved in P-time(stated in the ABSTRACT below). If you assume that P != NP then it can be observed that there is a greater market inefficiency when more data is present because it takes exponentially more time to compute.

https://arxiv.org/pdf/1002.2284.pdf

MikeDC

Apr 14 2020 at 3:42pm

My observation is that this criticism of EMH is consistent with the generally shallow understanding our “experts” have of data. My hypothesis is this is because “successful” research results are so dependent across almost all fields upon achieving “novel” results.

Because of this, experts dramatically overestimate small bits of novel or contrary evidence (such as the one time the stock mark was perceptibly “slow”) rather than the overwhelming but boring evidence that it’s largely correct.

This trend can also be seen in how experts have created so much misinformation around the use of masks. The straightforward evidence is masks are a low cost way to (strong evidence) prevent the wearer from spreading disease and (weaker evidence… in large part because it’s a boring subject with ethical problems) prevent the wearer from catching disease.

Instead of just going forward with this straightforward approach to mitigating risk, experts have gone to ridiculous extremes to argue some kind of Peltzman effect (risk compensating behavior) will overwhelm the risk mitigation activity.

But again, the evidence of this really isn’t warranted. Most studies of risk mitigation find that risk compensation, while present, erodes less than half of the direct effect of most activities. Sure, there’s the occasional idiot who thinks wearing a seat belt makes him invincible, but this guy is a minor exception, not the rule.

My concern is that experts have been conditioned to and increasingly operate as if the exceptions were the rules. They’re not. And we’re doing a grave disservice to everyone when we do this.

D.O.

Apr 14 2020 at 4:49pm

My uninformed guess is that “market” didn’t believe enough information from China. The thinking was along the lines “yes, another strange outbreak in East Asia; China as always is involved in some shenanigans with information, and who knows why they are doing it. Probably, not a big deal.” New thinking will probably be more nuanced, market participants will try to get a better sense in what is going on there and not simply ignore news from China as noise. EMH is supposed to work best when there are enough informed participants with enough money to make adjustments based on new information. I think the recent episode shown that there are not enough people working in financial speculations who understand China.

Matthew

Apr 15 2020 at 1:48pm

“EMH is supposed to work best…”

Is there a falsifiable definition of EMH out there somewhere?

Carl Futia

Apr 14 2020 at 8:13pm

I think the most useful version of EMH is the one which tells us that public information is reflected in market prices. But the views of Americans in China don’t qualify as public information. Nor does information about the situation in China qualify since the CCP did its best to suppress it.

Instead I suggest comparing the market price graph to information appearing in the New York Times or on the cable networks. You will find a pretty close correlation. So my interpretation of events says they are consistent with EMH. Sure, a few players had special insight (or luck) into upcoming events, just as they did prior to the housing crash. But the EMH does not exclude that possibility since those with special insight were a very small minority.

Matthew

Apr 14 2020 at 11:31pm

EMH is just preposterously wrong. Even congressmen do better than index investing.

Matthias Görgens

Apr 15 2020 at 5:28am

That’s a weird objection.

People in the American Congress use a lot of inside information in their trading.

There arguments against the EMH. This would only be an argument against some absurdly strong version of the EMH that no one holds.

Matthew

Apr 15 2020 at 1:46pm

If no one holds that version of EMH, perhaps they can bother to fix the definitions online in places like investopedia and Wikipedia:

https://www.investopedia.com/terms/e/efficientmarkethypothesis.asp

“The efficient market hypothesis (EMH), alternatively known as the efficient market theory, is a hypothesis that states that share prices reflect all information and consistent alpha generation is impossible. According to the EMH, stocks always trade at their fair value on exchanges, making it impossible for investors to purchase undervalued stocks or sell stocks for inflated prices. ”

https://en.wikipedia.org/wiki/Efficient-market_hypothesis

“The efficient-market hypothesis (EMH) is a hypothesis in financial economics that states that asset prices reflect all available information. A direct implication is that it is impossible to “beat the market” consistently on a risk-adjusted basis since market prices should only react to new information. ”

What version of EMH do you believe is defensible?

Ben

Apr 14 2020 at 11:32pm

What really kills the EMH: the company Zoom Technologies with the ticker ZOOM.

Matthias Görgens

Apr 15 2020 at 5:55am

That tells you that making short selling easier might be a good idea.

In unrelated news: of course, one of the first thing many European countries did was ban short selling.

Comments are closed.