Categories:

Efficient Markets Hypothesis

Finance

May 26 2021

Out of the mouths of Congressmen sometimes come gems. No one should ever be taxed twice on the same income. It's not fair and it's not just. So tweeted Jerry Nadler back in April. Nadler is a Democratic member of the U.S. House of Representatives. There's something to what he's saying. As I noted in my recent arti...

May 26 2021

The op-ed on vaccines and industrial policy written by Deirdre McCloskey and me for Project Syndicate prompted a very interesting comment from Dallas Weaver. It is on the Project Syndicate website, so I feel free in reprinting it below: On the claim of the government inventing the Internet, I am old enough to remember...

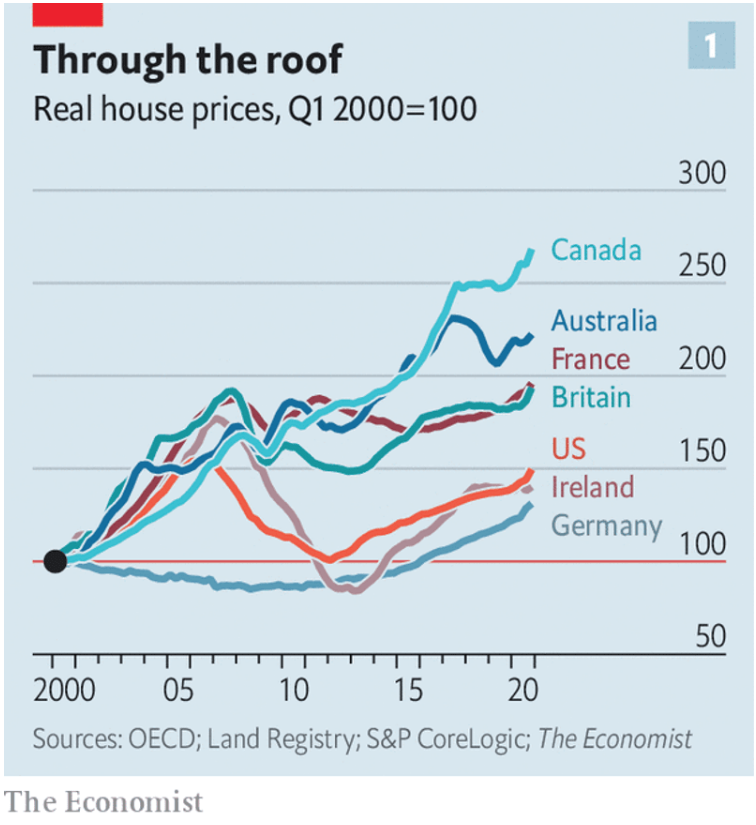

May 25 2021

When I started blogging in early 2009, I pushed back against the view that the housing market had gone through a "bubble". I pointed out that prices in countries such as Canada had risen as much or more than in the US, and yet had not crashed. Commenters told me, "you just wait, the Canadian market is starting to corre...

READER COMMENTS

Mike

May 25 2021 at 1:18pm

Living in California, I continue to be amazed at how quickly and strongly home prices have gone up over the past several years. The pandemic has dramatically accelerated pricing in “quality of life” locations like Tahoe and Santa Cruz. I suspect these sorts of markets will soften when people realize that “back to work” means, literally, going back to work, and a hour commute over mountain roads / owning and paying taxes on a second home starts to be a drag.

But I don’t know. I can’t quite figure out what’s going on. Certainly there’s very little supply relative to the demand, and this has a sort of self-fullfilling prophecy aspect to it given that people can’t sell their homes unless there’s somewhere to go – and the house they might be interested in buying is radically more expensive than their current home. (There’s also Prop 13, which really discourages selling one’s home in CA.)

Is a house on the California coast that was on the market for $2.2M last year now worth (per Zillow) nearly $4M? Have things fundamentally changed that much?

At some point, there just aren’t that many people – even in Silicon Valley – who can afford a $4M house. Right?

Scott Sumner

May 25 2021 at 8:17pm

The market knows best. If the market says those houses are worth $4 million, they are worth $4 million. BTW, I had a middle class job for most of my life (upper middle class in later years), and yet because of the rising stock market my 401k has more money than I expected to have. I bet there are many people who have made money in stocks, and then are using those funds to buy nice houses.

Of course that raises the issue of whether stocks are overpriced, but then the alternative is very low yield bonds. Ultimately, this is all related to the secular decline in long-term real interest rates. (Although of course it also matters why rates have fallen.)

Alan Goldhammer

May 25 2021 at 3:59pm

Perhaps you and Shiller should debate whether the term housing bubble was appropriate to describe what happened during the lead up to 2008. Certainly there was well documented culpability on the part of banks and shadow-banks whose lending standards resulted in loans that could not be serviced if the value of the underlying property could not be sold. The creation of exotic structured mortgage products that were purchased by unsuspecting rubes (both individual and institutional) was also contributory.

I remember reading this from one of Howard Marks (Oaktree Capital) newsletters written in mid-2010:

Housing prices were a factor but not the only one as any of us who were managing money both before and after the meltdown realize.

Scott Sumner

May 25 2021 at 8:23pm

You said:

“Certainly there was well documented culpability on the part of banks and shadow-banks whose lending standards resulted in loans that could not be serviced if the value of the underlying property could not be sold. ”

The issue of whether banks took excessive risks, or whether we should have had a different regulatory framework, is separate from the issue of whether housing was a bubble. It’s pretty clear that housing was not a bubble, but that doesn’t mean there aren’t moral hazard type issues with our financial system.

Kevin Erdmann’s looked at this issue more comprehensively than almost anyone else, and he finds little evidence that lax lending standards explain much of the housing boom of 2000-06. Indeed housing construction was actually pretty normal for an economic expansion during that period. Instead, growing NIMBY rules seem to be a bigger factor, which is why we are once again seeing high prices. Low interest rates combined with limits on new building put upward pressure on prices.

zeke5123

May 26 2021 at 9:37am

I don’t think you can describe institutional investors as “unsuspecting rubes.” AAA CDOs were trading with a lower price compared to traditional AAA debt (i.e., there was in fact a risk premium). Any basic investor understands that bond yields are based on two things: risk-free rate + risk premium. Yield is inversely related to price. Thus, the AAA CDOs in fact had a risk premium built into them. Certain institutional investors were required to hold certain quantum of AAA debt.

These investor managers took the opportunity to basically buy an asset that was riskier compared to what was supposed to be risked to drive more return. I wouldn’t call that unsuspecting (i.e., they had to know there was more risk or else there was a massive market inefficiency) as much as likely a P-A problem.

Steve X

May 25 2021 at 5:42pm

Zoning reform should be given great importance by Libertarians and Classical Liberals. Ed Glaeser’s work calculating the cost of zoning is great. It’s been replicted in many places as well.

In the 1970s the government regulated the price of flights, transport costs and so much more. One of the last areas where the government has similar control is zoning. Albeit with local government.

It’ll be really good when Bryan Caplan’s book about it comes out.

If supply were more elastic it’s unlikely the housing price rise would be so bad. Indeed, it’d be interesting to check what the house price rise is in the American Southwest where there is a lot of supply and fairly loose zoning compared to on the coasts.

Mind you, higher interest rates combined with the increase in remote work could lead to a drop in prices at some point.

Japan is, again the land of the future. Japanese house prices rose and rose. And then they didn’t at all for, what, 30 years? Mind you, Japan doesn’t have immigration to keep the population rising, as notably Canada and Australia do.

Scott Sumner

May 25 2021 at 8:26pm

Good comment. I’d add that Japan has surprisingly lax zoning. It’s odd that it’s hard to build in places with lots of land like Canada and Australia, and relatively easy in Japan.

Lizard Man

May 26 2021 at 1:15am

What are zoning policies and housing prices like in South Korea? How about the non-tier one cities in China?

Philo

May 26 2021 at 10:24am

The path of house prices over this period suggests that NIMBY has been even worse in Canada (and maybe also in New Zealand and Australia) than in the U.S. Is that your view, or are other factors more important for the Canadian case?

Scott Sumner

May 26 2021 at 2:06pm

I think it has been worse in those places, although I’m not certain.

Daniel Hill

May 26 2021 at 1:39pm

Since the start of the pandemic Australia has had a net population loss (no new immigrants, plus Australians deciding to permanently leave prison island) and the government is talking about border closure continuing another year. Yet the housing market has strengthened!

I own houses in the US and Australia. Every prediction I’ve made about these markets over the past 20 years has turned out to be wrong…

Mark Brophy

May 25 2021 at 6:21pm

I’m still waiting for the government to allow a free market in interest rates. When that happens, interest rates will rise sharply and real estate prices will fall sharply.

Scott Sumner

May 25 2021 at 8:27pm

Actually, there is a free market in interest rates. Even yields on corporate bonds are quite low.

Mark Brophy

May 27 2021 at 5:29pm

The Federal Reserve sets interest rates rather than the free market, forcing people to invest in stocks and real estate rather than something safe. It’s an enormous market distortion.

Jon Murphy

May 28 2021 at 4:00pm

Point of fact: the Fed does not, and cannot, set interest rates.

Jerry Brown

May 29 2021 at 2:59am

Point of fact- the Fed completely controls the rate of interest it pays on excess reserves. It completely controls the rate it will provide loans to banks short of reserves. It almost completely controls the Fed funds rate or the inter-bank rate on loans of reserves between banks. That is the base risk free rate of interest from which most else scales from including interest rates on US government bonds.

But it is true that the Fed cannot control whatever interest rate you might charge me if you wanted to lend me money.

Don Geddis

May 30 2021 at 2:18pm

The Federal Funds Rate is a free market rate. The Federal Reserve does not set the FFR; it only targets the FFR. There’s a huge difference between setting a price and targeting a price.

Thomas Lee Hutcheson

May 25 2021 at 6:36pm

One might argue that something about housing prices triggered the financial crisis of 2008. The recession was caused by the Fed failing to carry out it mandates and allowing aggregated demand to fall so much that prices and employment both declined. Pure malfeasance.

Phil H

May 25 2021 at 6:56pm

Here is one possible explanation: China. China still (despite the ‘ghost cities’) has an absolute shortage of housing; it’s urbanization + displacement compensation system created a massive class of people holding expensive assets; and it’s as big in terms of population as the entire developed world. It’s possible that China’s expansion created a massive demand shock that markets everywhere are still adjusting to.

Scott Sumner

May 25 2021 at 8:29pm

China probably played a role in some housing markets, but I suspect it’s only a modest fraction of the forces pushing up global asset prices.

And it’s not just Chinese “demand”, almost all of East Asia has high saving rates, which tends to depress global interest rates, raising asset prices.

marcus nunes

May 25 2021 at 9:17pm

From my latest post:

“…There´s no doubt, therefore, that the “Great Recession” was “Fed made”. Trying to put the blame on house prices (that´s supposed to have given rise to the “Financial Crisis”) is just shifting blame to make the Fed “look good”.

Did the Fed learn anything from that experience? Bernanke himself did not have to learn anything. The problem was that he had forgotten what he knew! Here´s what Bernanke knew long before becoming Fed chairman:

Bernanke (with Gertler & Watson) 1997 (on oil shocks)

Henri Hein

May 25 2021 at 11:08pm

Looking forward to it. Something that I noticed in the debate during and after the Great Recession was that almost everybody was ready to blame laissez-faire policies, for some reason. That struck me as ironic, since laissez-faire supporters had warned about the moral hazard problem for decades. I’m not saying moral hazard was the biggest factor behind the Great Recession. I don’t know that. It’s just a little fantastic that since this was exactly the kind of event you would expect if the moral hazard problem is real, that it should then be completely ignored in the aftermath.

Scott Sumner

May 26 2021 at 2:08pm

I agree about moral hazard being a problem that contributed to the banking crisis. I hope my book will dissuade people from believing that the Great Recession was caused by laissez-faire policies.

Thomas Lee Hutcheson

May 27 2021 at 7:32am

Hopefully it will separate the issues of which (if any) policy failures triggered the 2008 financial crisis from those (mainly by the Fed although the reluctance/inability of governments to invest according to an NPV rule also contributed) that explain the recession of 2008-2020.

MarkW

May 26 2021 at 7:42am

The real house price chart indicates that NIMBYism is a significantly smaller problem in the U.S. than most of the developed world. Yay us!

Also, as far as bubbles go, if we go back to ’86:

https://public.tableau.com/shared/R5MMXNHDP?:display_count=y&:origin=viz_share_link&:embed=y

It sure looks to me that that we have an overall trend-line with a 2006 bubble. Many U.S. markets still haven’t reached the peak (in real terms) that they hit in 2006. I wouldn’t think that to declare a bubble, you’d need housing prices to fall precipitously and stay there for ever — falling precipitously and taking 15 years to recover would be more than enough. Looking at the very long term chart:

https://www.longtermtrends.net/home-price-vs-inflation/

2006 still looks like the peak of a bubble — a deviation from the long term CPI trend line much greater than any other in our history. And 2021 is looking pretty similar. How surprised would we be by a post-2006 repeat — a very sharp decline followed by a period of a decade or two before prices again recovered?

Look at Miami. In 2000 it was at 100. By 2006 it was at 239. By 2011 it was back down to 102. That wasn’t a bubble?

Scott Sumner

May 26 2021 at 2:10pm

You asked:

“That wasn’t a bubble?”

No. Asset prices are volatile even in non-bubble markets.

Brian Donohue

May 26 2021 at 11:39am

Good post, but I don’t know what “almost all assets are expensive” means. Compared to what? If all assets are expensive, are any assets expensive?

It seems to me that “guarantees” have been getting more expensive. It started with Treasuries, moved to corporate bonds, and now I reckon stocks of big companies with stable earnings have become more expensive, but if earnings forecasts are to be trusted, the overall stock market does not look very expensive compared to alternatives today.

Scott Sumner

May 26 2021 at 2:11pm

You asked:

“Compared to what?”

Compared to income flows (rents, dividends, interest payments, etc.)

Brian Donohue

May 26 2021 at 4:26pm

OK, seems like a long way around the block to say that interest rates are low and that low rates are reflected in the price of all financial assets.

AMT

May 26 2021 at 4:41pm

So if bubbles don’t exist, you don’t think that Gamestop stock is significantly overvalued right now?

Scott Sumner

May 27 2021 at 1:40pm

I have no idea what Gamestop is worth. My point is that bubble theories have not proven useful to investors.

AMT

May 27 2021 at 7:03pm

Logically, then, you must actually think Gamestop is worth whatever it is currently trading for, that’s EMH.

I don’t think you can say “bubble theories are not useful”; they’re just saying something is overvalued, which is obviously a useful concept. The problem is many people are often very overconfident with their assessments and make bad predictions all the time. In that sense, of course you shouldn’t believe many of the people who assert that something is a bubble because a lot probably have no clue what they’re talking about. Of course there will always be business journalists claiming DEFINITELY GIANT BUBBLE because it brings in clicks. It’s literally their job to act like they know with great certainty things they are basically guessing about, because people don’t want to hear a bunch of “maybes” in those types of articles, and there’s very little downside to being wrong.

It’s a bit like saying “medical doctors are not not useful” because there are a lot of moronic chiropractors out there selling snake oil. You should expect a lot of the people claiming there are bubbles to be wrong, but that doesn’t mean bubbles don’t exist or that they aren’t a useful concept. I think the Gamestop stock is a pretty good example of a very likely bubble. EMH is an excellent starting point that will approximate the market very well much of the time, but sometimes people DO invest in an irrational and unsustainable way.

robc

May 28 2021 at 3:11pm

I don’t think GME is irrational. A large chunk (in terms of investors, not dollars invested) of the investors are planning to stay long until the shorts cash out, preferably by going bankrupt. They want to watch the Citadel (the hedge fund, not the university) burn.

We may not agree with them, but it is rational. Unsustainable? Depends on the goal, doesn’t it? To outlast the shorts? Yeah, they might be able to pull it off.

I agree with you about bubbles, but not sure GameStop is a good example.

Michael Rulle

May 27 2021 at 10:44am

I like looking at California for empirical data on housing as it was “ground zero” for what was a housing crash.

For all practical purposes, however, the housing crisis had ended by Spring of 2008—-as annualized monthly sales began to increase again—each month was higher than previous until it doubled by September 2008.

Interestingly growth in sales stabilized in March of 2009 when median Housing prices reached the bottom (also when the stock market hit bottom in 2009)—40% lower than 1 year earlier. And less than half the peak.

California existing median sales prices are now at all time high-800k+ ( 33% higher than pre-Great recession peak), have been up 7-8 months in a row—-and annualized monthly growth in sales (65%) have reached a 12 year high. (As of April—see (car.org)

Under the “bubble theory of markets”——we should be in for a super crash. Bigger than ever! No one is mentioning California housing market crashing however. In fact, forecasts are mostly moderate increase.

‘I look forward to your book as well—-

Comments are closed.