Gross Domestic Product

By Lincoln Anderson

In addition, the Commerce Department derives data on inputs to production (labor and capital) and tabulates them to form industry data on production; intermediate steps in production (input-output tables); detailed data on prices; and international and regional statistics. The theoretical development and construction of this accounting system was a major achievement requiring the services of a renowned group of accountants, business executives, economists, and statisticians. And because the economy continues to evolve, the conceptual and statistical work is never complete. Government agencies are continuously revising the data and occasionally find sizable errors in GDP or GDP components. Keeping GDP current and accurate is no mean feat.

For the United States, GDP replaces gross national product (GNP) as the main measure of production. GDP measures the output of all labor and capital within the U.S. geographical boundary regardless of the residence of that labor or owner of capital. GNP measures the output supplied by residents of the United States regardless of where they live and work or where they own capital. Conceptually, the GDP measure emphasizes production in the United States, while GNP emphasizes U.S. income resulting from production. The difference, called net factor income received from abroad, is trivial for the United States, amounting to only $13 billion (0.2 percent of GDP) in 1991. This shift in emphasis brings the United States into conformance with the international accounting convention.

GDP measures production, not exchange. If economists, policymakers, and news commentators kept this simple truth in mind, much confusion over the interpretation of economic statistics might be avoided. Many proposals to cut taxes, for example, are aimed at “stimulating consumer spending,” which is expected to cause an increase in GDP. But consumer spending is a use of GDP, not production. A rise in consumer demand could simply crowd out investment, not raise GDP.

Unfortunately, the GDP data are usually presented in a format that emphasizes exchange (the use of GDP) rather than production (the source of GDP). GDP is represented as the sum of consumer spending, housing and business investment, net exports, and government purchases. Behind this accounting façade lurks the truth: GDP is generated by individual labor combined with both proprietors’ and business capital, raw materials, energy, and technology in a myriad of different industries. The Bureau of Economic Analysis (the agency within the Department of Commerce that is responsible for GDP statistics) does show these relationships in the input-output tables and in the GDP-by-industry data tables (now produced annually). But most economists and the press focus on the uses of GDP rather than these presentations of GDP as production.

For better or worse, the different formats do influence how people think about the sources of economic growth. Which, for example, is more of a driving force in the economy—retail sales or growth in the labor force? Are inventory levels a key factor at turning points in the business cycle, or is prospective return on investment the key? Does higher government spending increase GDP, or do lower marginal tax rates? Are higher net exports a positive or a negative factor? In answering these questions, Keynesians usually emphasize the first choice while supply-siders place more weight on the second.

In the short run, in business cycles the Keynesian emphasis on demand is relevant and alluring. But heavy-handed reliance on “demand management” policies can distort market prices, generate major inefficiencies, and destroy production incentives. India since its independence and Peru in the eighties are classic examples of the destruction that demand management can cause. Other less developed countries like South Korea, Mexico, and Argentina have shifted from an emphasis on government spending and demand management to freeing up markets, privatizing assets, and generally enhancing incentives to work and invest. Rapid growth of GDP has resulted (see Third World Economic Development).[

In the United States the debate over the sources of economic growth can be informed by GDP statistics. Take three examples over the past decade. First, there has been a lot of handwringing over the supposed decline in U.S. manufacturing. Based on declining employment in manufacturing, many commentators asserted throughout the eighties that the United States was “deindustrializing.” It certainly is true that employment in manufacturing fell from a peak of 21 million workers in 1979 to 19 million by 1990. But the GDP data show that the production of goods in the United States was rising rapidly after the 1982 recession and, by 1989, hit a ten-year high as a share of total GDP. The decline in manufacturing employment was more than offset by surging productivity. The rebuilding of U.S. manufacturing in the eighties occurred at the same time that many politicians and some economists were convinced we had given up our competitive position in world markets. A cursory glance at the GDP production data would have revealed the error.

Second, many people have viewed the rise in imports in the eighties with similar alarm. I believe that fear is groundless and is based on accounting rather than economics. With all other components of GDP held constant, a one-dollar increase in imports necessarily means a one-dollar drop in GDP. But—and this is something that simple accounting cannot tell us but that economics does—all other things are not equal. Rapid growth in GDP is generally associated with a large rise in imports. The reason is that high demand for foreign products coupled with high rates of return on domestic investment tends to pull foreign investment into a country and increase imports. The eighties were no exception: imports and the trade deficit surged concurrently with fast growth in GDP. Despite the lack of historical support for the proposition that imports reduce GDP, and despite strong opposition from economists stretching back to Adam Smith, protectionist trade policies were advocated and to some degree implemented in the eighties to “solve” the “problem.” A closer look at the correlations between GDP and imports might have dispelled some of the mercantilist myths that protectionists raised (see Mercantilism).

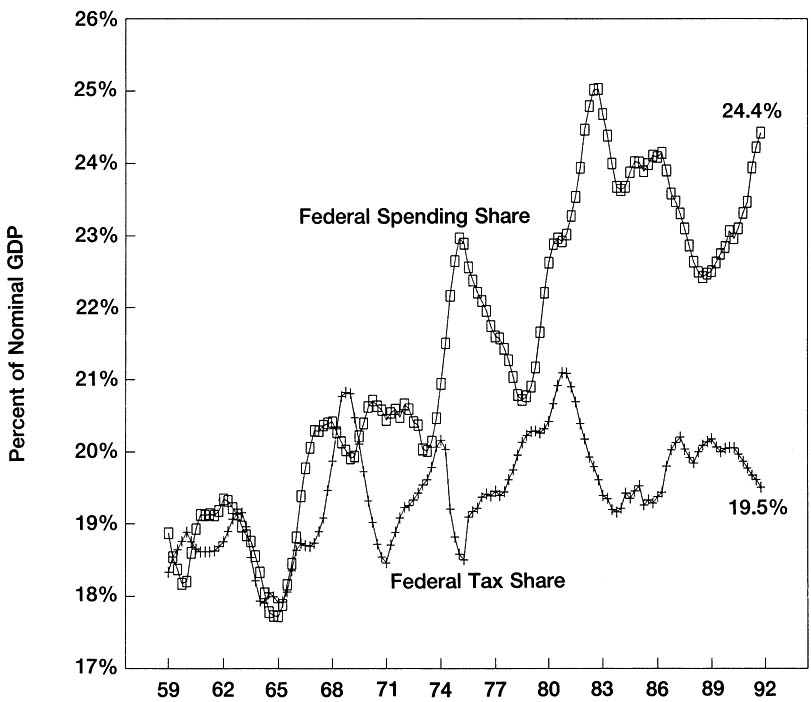

Third, there is the controversy over the cause of the federal budget deficit. In the eighties, when the budget deficit ballooned to over $200 billion, a prolonged debate ensued over whether the rise in the deficit was caused by spending growth or tax cuts. One way to cut through the haze of numbers and get at the simple truth is to look at total federal receipts and outlays as shares of GDP. Federal tax receipts as a share of GDP did dip from a high of 21 percent in 1981 to 19 percent in the mid-eighties, but they have since climbed back to about 20 percent. With current tax receipts now high as a share of GDP, it is clear that major tax “cuts” have not occurred and that higher government spending is largely responsible for the budget deficit.

Chart 1. Federal Spending and Taxes as GDP Shares Four-Quarter Average:

1960 to 1992

SOURCE: Bureau of Economic Analysis.

Enlarge in new window

The United States revises its base year about every five years. The base year for real GDP was recently moved up from 1982 to 1987. As a result “real” GDP growth over the eighties was revised down slightly. The Soviet Union took much longer to revise its base year. Until the sixties the Soviets used 1928 as the base year for computing “real” GDP. Therefore, published data on growth rates were biased upward by a large percentage, and the underlying weakness in the Soviet economy was obscured. The Bureau of Economic Analysis (BEA) plans to publish a measure of real GDP and major components using a shifting base year. This measure will provide a more accurate representation of growth in years far from the 1987 base period. I strongly recommend sliding base (or “chain”) measures in studies using a decade or more of real GDP data.

In practice BEA first uses the raw data on production to make estimates of nominal GDP, or GDP in current dollars. It then adjusts these data for inflation to arrive at real GDP. But BEA also uses the nominal GDP figures to produce the “income side” of GDP in double-entry bookkeeping. For every dollar of GDP there is a dollar of income. The income numbers inform us about overall trends in the income of corporations and individuals. Other agencies and private sources report bits and pieces of the income data, but the income data associated with the GDP provide a comprehensive and consistent set of income figures for the United States. These data can be used to address important and controversial issues such as the level and growth of disposable income per capita, the return on investment, and the level of saving.

In fact, just about all empirical issues in macroeconomics turn on the GDP data. The government uses the data to define emerging economic problems, devise appropriate policies, and judge results. Businesses use the data to forecast sales and adjust production and investment. Individuals watch GDP as an indicator of well-being and adjust their voting and investment decisions accordingly. This is not to say that the GDP data are always used or used wisely. Often they are not. Nor are the GDP data perfect. But ignoring the GDP data is as close as one can come in macroeconomics to ignoring the facts. And that is a perilous practice.

Lincoln Anderson is the managing director and chief investment officer of LPL Financial Services in Boston. He was previously the economist at Fidelity Investments in Boston and, before that, was a senior economist at the Council of Economic Advisers from 1982 to 1986.

Fox, Douglas R., and Robert Parker. “The Comprehensive Revision of the U.S. National Income and Product Accounts: A Review of Revisions and Major Statistical Changes.” Survey of Current Business 71, no. 12 (December 1991): 24-42.

“Gross Domestic Product as a Measure of U.S. Production.” Survey of Current Business 71, no. 8 (August 1991): 8.

Jaszi, George, ed. “The Economic Accounts of the U.S.: Retrospect and Prospect.” Survey of Current Business 51, no. 7 (July 1971).

Young, Allan H. “Alternative Measures of Real GDP.” Survey of Current Business 69, no. 4 (April 1989): 27-34.

Related Links

Robert P. Murphy, Pitfalls in GDP Accounting. Econlib, November 2016.

David R. Henderson, GDP Fetishism. Econlib, March 2010.

Diane Coyle on GDP, EconTalk, April 28, 2014.

Martha Nussbaum on Creating Capabilities and GDP, EconTalk, September 29, 2014.

GDP, Econlib College Economics Topics.