Demand

A High School Economics Guide

Supplementary resources for high school students

Definitions and Basics

Demand, from the Concise Encyclopedia of Economics

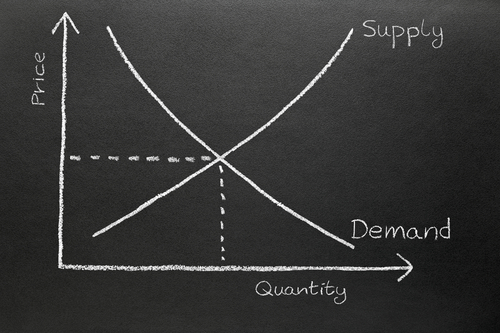

One of the most important building blocks of economic analysis is the concept of demand. When economists refer to demand, they usually have in mind not just a single quantity demanded, but what is called a demand curve. A demand curve traces the quantity of a good or service that is demanded at successively different prices.

The most famous law in economics, and the one that economists are most sure of, is the law of demand. On this law is built almost the whole edifice of economics. The law of demand states that when the price of a good rises, the amount demanded falls, and when the price falls, the amount demanded rises….

Law of Demand Interactive Lesson Plan, from Marginal Revolution University.

Demand, Supply, and the Market Lesson Plan, from the Foundation for Teaching Economics.

This lesson focuses on suppliers and demanders, the participants in markets; how their behavior changes in response to incentives; and how their interaction generates the prices that allocate resources in the economy.

Microeconomics, from the Concise Encyclopedia of Economics

The strength of microeconomics comes from the simplicity of its underlying structure and its close touch with the real world. In a nutshell, microeconomics has to do with supply and demand, and with the way they interact in various markets….

Morgan Rose, Elasticity and its Expansion. Econlib, January 2003.

In economics, an elasticity is a measurement of the responsiveness of one variable to a change in another variable. There are many different types of elasticities distinguished by the pair of variables that each one considers, but at their core they are all simply comparisons of how one thing changes in response to changes in another.

In the News and Examples

Richard McKenzie, How Free Market Kidney Sales Can Save Lives- And Lower the Total Cost of Kidney Transplants. Econlib, March 2012.

The demand for kidneys is a function of several factors, including the size of medical schools and their need for kidneys in research and instruction and the number of people who experience kidney disease or outright failure. Because kidney failures can be linked to a person’s eating and drinking habits, such habits can also affect the demand for kidneys. Further, the demand for kidneys is related to the cost of alternative treatments (dialysis, for example) and known techniques for transplanting organs.

A Little History: Primary Sources and References

Indifference curves, diminishing marginal utility, and the demand curve: Gradations of Consumers’ Demand, Book III, Chapter III from Principles of Economics, by Alfred Marshall

There is an endless variety of wants, but there is a limit to each separate want. This familiar and fundamental tendency of human nature may be stated in the law of satiable wants or of diminishing utility thus:—The total utility of a thing to anyone (that is, the total pleasure or other benefit it yields him) increases with every increase in his stock of it, but not as fast as his stock increases. If his stock of it increases at a uniform rate the benefit derived from it increases at a diminishing rate. In other words, the additional benefit which a person derives from a given increase of his stock of a thing, diminishes with every increase in the stock that he already has.

Fred McChesney, Armen Alchian: An Economist Lion in Winter. Econlib, November 2009.

If time is important on the supply side, what of the demand side? Here, too, Alchian’s work has been pathbreaking. In particular, he (with co-author William Allen) pioneered recognition of the Second Law of Demand.

Advanced Resources

The Magic of Markets: Trade Creates Wealth Lesson Plan, from the Foundation for Teaching Economics.

Trade is the voluntary exchange of goods and services. People engaging in trade must be willing to bear a cost (give up something). Therefore, we know that people will only participate voluntarily when they expect to gain from the exchange. If even one of the trading partners believes he cannot gain, the exchange will not take place.

Richard McKenzie, Market Competitiveness and Rationality: A Brain-Focused Perspective. Econlib, October 2019.

Neoclassical economists start their analytics by assuming that resource scarcity is pervasive, and people are the ultimate seat of rational decision-making. The scarcity problem, however, is not taken into consideration within the human brain, given neoclassicists’ perfect-rationality premise, which makes decision refinements costless.